Click to enlarge

The quarter the numbers started to agree

For three years, Metro Vancouver commercial real estate has sent mixed signals. Leasing softening in one asset class while another held firm. Cap rates drifting. Sentiment cautious. Every quarter had at least one sector pulling against the others.

Q1 2026 is the first quarter where the leasing data, the transaction data, and the sentiment data are all moving the same direction.

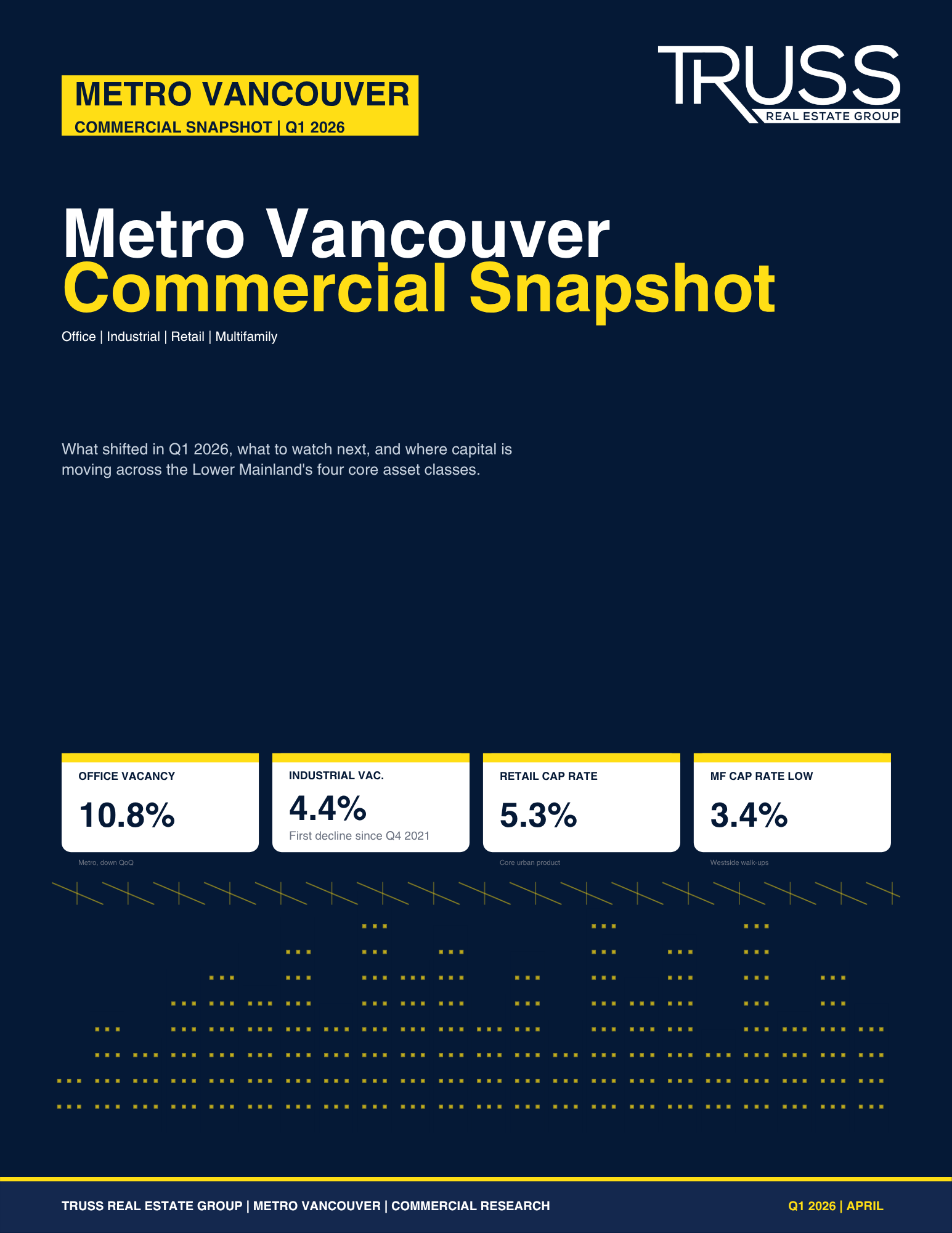

Office vacancy down. Industrial availability down for the first time since Q4 2021. Westside apartment cap rates compressing back below 4%. Core urban retail holding at sub-5.5% caps on well-leased product. Investor conviction — measurable in the depth of bids on quality product — is returning.

This isn’t a boom. It’s a floor being established. For investors, occupiers, and owners who have been waiting for a cleaner read on the market, Q1 2026 delivered one.

Metro Vancouver commercial real estate at a glance — Q1 2026

| Asset class | Q1 2026 headline metric | Direction |

|---|---|---|

| Office | 10.8% vacancy (Metro) | Down from 10.9% QoQ |

| Industrial | 4.4% vacancy | First QoQ decline since Q4 2021 |

| Retail | 2–4% vacancy (ex-regional malls) | Stable / landlords holding firm on rent |

| Multifamily | 3.4% to 4.9% cap rate range on traded product | Westside compressing |

Metro Vancouver total CRE dollar volume fell 8.3% in 2025 to roughly $7.5B (from $9.7B in 2024), with that softness carrying into early Q1. But the composition of deals shifted meaningfully toward quality — a flight to core, not a broad retreat.

Office: a turning point, led by quality

Downtown Class A is carrying the recovery.

Metro Vancouver’s office market has now posted two consecutive quarters of positive net absorption — the first time that’s happened since 2022. Downtown vacancy fell to 12.3% from 12.8%, and downtown Class A vacancy sits at its lowest level since Q3 2022. Suburban nodes (Burnaby, Richmond, Surrey) delivered the largest vacancy drop in aggregate, falling to 9.1%.

The City of Vancouver’s ~52,000 SF lease at 1125 Howe Street — housing approximately 500 staff — was one of the quarter’s largest downtown commitments and a clean signal of the broader theme: tenants that delayed decisions in 2024-25 are returning with real, sized requirements.

Class B is a different story. Across every submarket, Class B buildings continue to face pressure and will require capital repositioning to compete in an increasingly K-shaped leasing market. The gap between A and B product is wider than it’s been in a decade.

What we’re watching: the Broadway submarket is the next real test. Several new buildings are delivering in 2026 with major occupiers already committed, but the market hasn’t yet absorbed tenant depth outside the downtown core. Cadillac Fairview’s revised proposal for a 22-storey downtown tower is a genuine institutional vote of confidence — the clearest long-term signal we’ve seen in two years.

Industrial: the supply cycle ends

After 12 straight quarters of rising vacancy, Metro Vancouver industrial finally turned. Overall vacancy edged down 10 bps to 4.4% — small on paper, but the first quarterly decline since Q4 2021 and a meaningful psychological reset for occupiers and investors. Net absorption was positive for the fifth consecutive quarter at +263,000 SF.

Large-format demand is driving the shift. Twelve requirements over 100,000 SF are currently under offer or contract in Metro Vancouver. We expect available big-box inventory to be cut roughly in half by Q2, with rent stabilization likely by late Q2 into Q3. Mid-bay and flex product continues to trade at more competitive terms — that’s where tenants still have leverage, and where sharp buyers can find value.

Vancouver led all Canadian markets outside Toronto for Q1 industrial construction starts at 1.4M SF, reinforcing the region’s long-term structural demand story. The pipeline is thinning and demand is rebuilding — historically that combination sets up a clean runway for rent recovery through the back half of the year.

Takeaway for investors: the window for buying stabilized Metro Vancouver logistics at 2025 pricing is closing faster than most underwriting models assume.

Retail: stable fundamentals, a luxury supply wave

Retail entered 2026 as the region’s most structurally stable asset class. High-street, neighborhood, service-oriented, and power centre formats all sit in a tight 2–4% vacancy band, and landlords are holding firm on rents.

The quarter’s headline trade — the air-space parcel at 1101-1133 Alberni Street, home to the Park Hyatt’s ground-floor retail — closed at $55M, or $1,342 per square foot at a 5.3% cap rate. That transaction re-sets the benchmark for luxury-adjacent urban retail in Vancouver. At the other end of the spectrum, Langley product continues to trade in the high $300s per square foot, a spread that reflects the ongoing premium for core urban high-street positions.

Oakridge Park is the retail story of the year. Roughly 650,000 SF of new retail anchored by global luxury, fashion, and lifestyle brands opens this spring — Vancouver’s first major mall delivery in over a decade. We expect it to reshape the city’s retail hierarchy and draw new footfall patterns through the central corridor, with secondary effects on Alberni Street pricing, Oakridge-adjacent residential, and Cambie Corridor retail leasing.

The asterisk is regional malls, where the return of Hudson’s Bay space is creating temporary vacancy to work through in 2026. Several mall landlords are already in active anchor negotiations — expect resolution during the back half of the year.

Where private capital is active: suburban medical, grocery-anchored, and service retail continue to attract strong private-capital bids. That’s the quiet, high-conviction trade of the quarter.

Multifamily: core tightens, CMHC leverage returns

Apartment pricing firmed up in Q1. Westside Vancouver product is trading at or below 4% cap rates again.

The quarter’s marquee trade was a 14-unit walk-up at 2250 York Avenue in Kitsilano at a 3.4% cap rate and $428,000 per door — the tightest apartment cap of the quarter. The largest Q1 multifamily trade was a newer 31-unit mixed-use building at 727 East 17th Avenue: $12.5M, $694,000 per unit, 4.4% cap.

The broader picture is nuanced. 2025 dollar volume fell 24%, but the number of buildings sold actually rose 2%. That’s a flight to smaller, CMHC-financeable deals — not a retreat from the asset class.

With debt availability improving and purpose-built rental vacancy at 3.7% (the highest since 1988, per CMHC’s 2025 report), underwriting is shifting away from pure rent-growth bets toward income durability and replacement-cost dynamics. We expect a meaningful pickup in $10–30M apartment trades as CMHC-insured debt flows rebuild through the year.

How Truss reads Q1 2026

Three themes are worth carrying into Q2.

1. Quality is pulling away from everything else. Downtown Class A, core urban retail, Westside apartments — the top of each asset class is posting the strongest numbers. Class B office, regional malls, and suburban flex industrial are working through harder adjustments. Underwriting has to respect the spread between A and B product more than it did in 2022.

2. Debt is reopening. CMHC-insured multifamily is the clearest signal, but conventional industrial and retail financing is widening again as well. Deals that were stuck in 2024-25 because of underwriting gaps are penciling at current spreads. Borrowers who sat on the sidelines should be re-running their numbers.

3. The floor is real, but this isn’t a 2021 reboot. Vacancy rates remain well above the cycle lows. Construction starts are slowing. Rent growth through 2026 will be modest, not explosive. The opportunity set is for disciplined buyers with sharp submarket views — not broad-index bets.

Q2 2026 outlook

A constructive setup. We expect industrial vacancy to tighten further, office fundamentals to continue improving in Class A, Oakridge Park to reshape retail footfall across the central corridor, and apartment transaction volume to rebuild as CMHC-insured debt flows increase. Watch for the first material rent stabilization in big-box industrial by late Q2.

Download the Full Q1 2026 Snapshot

The full 7-page Metro Vancouver Commercial Snapshot includes every figure referenced above, expanded submarket detail across office, industrial, retail, and multifamily, and every notable deal from the quarter.

Talk to Truss

Truss Real Estate Group is a specialized commercial advisory based in Metro Vancouver, covering office, industrial, retail, and multifamily across the Lower Mainland and Fraser Valley. We publish a snapshot like this every quarter — and we spend the rest of our time helping owners, investors, and occupiers turn market data into decisions.

If you’re working on an acquisition, a disposition, a lease, or a portfolio question, we’d welcome the conversation.

Stathis Michael Savvis PREC* · Co-Founder Real Estate Advisor, Stonehaus Realty Corp. 604-897-8974 · [email protected]

Amrita Guram · Co-Founder Real Estate Advisor, Stonehaus Realty Corp. 604-518-9101 · [email protected]

trussrealestate.ca

Sources: CBRE, Colliers, Avison Young, Cushman & Wakefield quarterly market reports; CMHC 2025 Rental Market Report; Altus Group investment data; vancouvermarket.ca; Business in Vancouver; Daily Hive. All figures published April 2026. E.&O.E.